The global market for optometry equipment is experiencing robust growth, projected to expand from $4.5 billion in 2024 to $6.1 billion by 2029 at a compound annual growth rate (CAGR) of 6.4%. This burgeoning industry is fueled by several key drivers, including an aging population, the rising prevalence of eye disorders, and continuous technological advancements in ophthalmic devices.

Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=14475790

A Closer Look at Market Dynamics

The escalating incidence of eye conditions such as cataracts, glaucoma, and age-related macular degeneration is a primary catalyst propelling the demand for optometry equipment. As people grow older, particularly beyond the age of 60, the risk of these vision-impairing diseases increases, necessitating accurate diagnosis and treatment facilitated by advanced ophthalmic technologies.

However, the high cost of optometry equipment and the adoption of refurbished devices pose a significant restraint on market growth. The substantial investment required for purchasing, maintaining, and operating these sophisticated machines can be prohibitive, especially for smaller clinics and diagnostic facilities.

Emerging Opportunities and Challenges

While developed nations dominate the current optometry equipment landscape, emerging economies like South Africa, Brazil, Turkey, Russia, India, and South Korea present lucrative growth opportunities. Factors such as a high prevalence of eye diseases, a large patient base, improving healthcare infrastructure, rising disposable incomes, and the burgeoning medical tourism sector in these regions make them attractive markets for industry players.

Conversely, low awareness and limited accessibility to eye care services in low-income economies pose a significant challenge. Rural populations in countries like India, Saudi Arabia, Israel, Kenya, and South Africa often lack adequate knowledge about eye disorders and face restricted access to cutting-edge optometry equipment, hampering market penetration.

Market Segmentation and Key Players

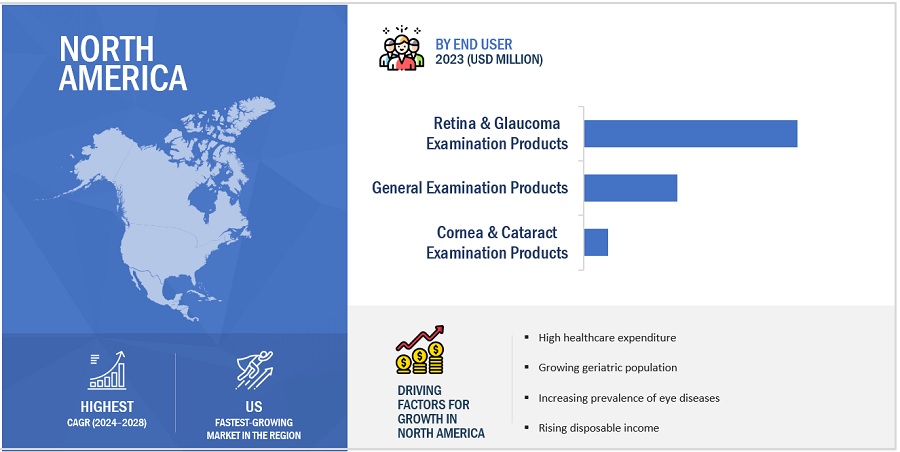

The optometry equipment market is segmented by product type, application, end-user, and region. In 2023, the retina and glaucoma examination products segment held the largest share, driven by advancements in diagnostic technologies and the increasing prevalence of these conditions. The general examination segment dominated in terms of application, fueled by the rising incidence of diabetes, hypertension, and other infections that can affect vision.

Geographically, North America emerged as the leading region in 2023, attributed to its aging population, high prevalence of ocular diseases, access to advanced equipment, and widespread adoption of ophthalmology procedures and treatments.

The market is moderately consolidated, with key players such as Carl Zeiss Meditec AG, Alcon, EssilorLuxottica, Topcon Corporation, and Bausch Health Companies Inc. commanding a significant market share. These industry giants leverage their extensive product portfolios, global reach, robust marketing and distribution networks, substantial research and development budgets, and well-established brand recognition to maintain their market dominance.

As the optometry equipment market continues its upward trajectory, driven by demographic shifts, technological innovations, and the rising burden of eye diseases, it presents ample opportunities for established players and new entrants alike to capitalize on this growing demand for vision care solutions.

Leave a comment