-

Technology in Home Healthcare: Driving Efficiency and Quality Care

The global home healthcare market is poised to achieve significant growth, expected to soar to USD 383.0 Billion by 2028 from USD 250.0 Billion in 2023, indicating a robust CAGR of 8.9% during the forecast period. This growth trajectory is primarily propelled by the expanding elderly population and the increasing prevalence of chronic ailments.

Key Market Players:

Leading players in the market include Fresenius SE & Co. KGaA (Germany), Abbott (US), GE HealthCare (US), Koninklijke Philips N.V. (Netherlands), ResMed, Inc. (US), among others. These key industry participants are strategically employing various tactics to steer the global growth trajectory of the home healthcare sector.

Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=696

Fresenius SE & Co. KGaA (Germany):

Fresenius SE & Co. KGaA (Germany) secured the top position in the home healthcare market in 2022, commanding a 4.7% market share. The company has cemented its leading status through robust distribution networks spanning North America, Europe, Latin America, Asia Pacific, and Africa. Fresenius boasts both direct and indirect distribution channels globally and pursues a blend of organic and inorganic growth strategies. Notably, the company expanded its home hemodialysis product offerings in Europe, the Middle East, and Africa in May 2020. Additionally, in August 2022, Fresenius acquired InterWell Health Brand (US), augmenting its expertise in kidney care value-based contracting and performance.

Abbott (US):

Abbott (US) captured a 3.9% share of the home healthcare market in 2022, leveraging its expanding global sales and distribution network. The company prioritizes research and development endeavors to develop and produce innovative products, enhancing its competitive edge. Abbott’s substantial investments in R&D fortify its product portfolio and distribution strategies, positioning it favorably for future growth. Moreover, Abbott pursues strategic acquisitions to bolster its market presence, exemplified by its collaboration with Insulet Corporation (US) in June 2020 to integrate Abbott’s CGM technology with Insulet’s Omnipod Horizon Automated Insulin Delivery System, providing tailored automated insulin delivery and care solutions for individuals with diabetes.

Global Home Healthcare Manufacturers:

Prominent manufacturers in the home healthcare industry include Philips Healthcare (Netherlands), Medtronic plc (Ireland), Omron Healthcare, Inc. (Japan), Fisher & Paykel Healthcare Limited (New Zealand), Bayer AG (Germany), Roche Diagnostics (Switzerland), Becton, Dickinson and Company (BD) (United States), among others. These companies specialize in offering a diverse array of home healthcare products and solutions, spanning medical devices, monitoring equipment, diagnostic tools, and other tailored healthcare products for home use.

Philips Healthcare (Netherlands):

Philips Healthcare leads the global home healthcare solutions market, offering an extensive range of medical devices and equipment designed to facilitate at-home health management. From sleep apnea therapy devices to remote patient monitoring solutions, Philips’ innovative offerings empower individuals to monitor and manage their health conditions conveniently.

Medtronic plc (Ireland):

Renowned for its medical technologies and solutions, Medtronic plc provides a wide array of home healthcare products aimed at enhancing patient outcomes and quality of life. With a focus on innovation and patient-centricity, Medtronic’s portfolio includes insulin pumps, continuous glucose monitoring systems, and other devices tailored for managing chronic conditions at home.

Omron Healthcare, Inc. (Japan):

A leading manufacturer of home healthcare devices, Omron Healthcare, Inc. emphasizes wellness promotion and disease prevention. Its product lineup encompasses blood pressure monitors, nebulizers, thermometers, and activity trackers, empowering individuals to monitor vital health parameters and make informed decisions about their health.

Fisher & Paykel Healthcare Limited (New Zealand):

Specializing in respiratory care products and sleep apnea therapy devices, Fisher & Paykel Healthcare Limited prioritizes patient comfort and compliance. Its offerings include humidification systems, nasal masks, and CPAP devices, tailored to meet diverse patient needs worldwide.

Bayer AG (Germany), Roche Diagnostics (Switzerland), Becton, Dickinson and Company (BD) (United States):

These global healthcare giants offer a wide range of consumer health products and medical devices for home use, spanning blood glucose meters, self-testing kits, insulin syringes, pen needles, lancets, and more, empowering individuals to manage their health conditions effectively at home.

-

Exploring Market Dynamics and Growth Opportunities in Oligonucleotide Synthesis: A Comprehensive Study

According to a new report by MarketsandMarkets™ – Oligonucleotide Synthesis Market in terms of revenue was estimated to be worth $8.8 billion in 2024 and is poised to reach $19.7 billion by 2029, growing at a CAGR of 17.5% from 2024 to 2029.

One of the key factors driving the market growth is the growing acceptance of alternate therapies such as oligonucleotide-based therapies for the treatment of neurological and rare The incorporation of synthesized oligonucleotides to treat various diseases also supports market growth.

Download an Illustrative overview: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=200829350

Probes are an important subsegment in the market for synthesized oligonucleotides. The segment accounted for the second-largest market share of the synthesized oligonucleotide market. This is due to high specificity and sensitivity of probes allowing their use in genetic research, pathogen detection, clinical diagnostics, and the study of gene expression patterns, offering insights into diverse biological processes and disease mechanisms. Techniques such as fluorescence in situ hybridization (FISH) utilize these probes for the detection of various genetic abnormalities that the root cause of several birth defects, neurological conditions and cancers among others.

By end user, hospitals accounted for the largest share of the oligonucleotide synthesis market in 2023. Growth in this market is largely driven by the significant number of FDA-approvals for oligonucleotide-based drugs especially antisense oligonucleotide drugs for rare and neurological diseases, increasing awareness towards alternative therapies and growing health-care spending. Ongoing research to develop oligonucleotide-based drugs for more common diseases such as cardiovascular diseases, supported by availability of reimbursement policies in developed economies are aiding this segment’s growth.

In 2023, PCR accounted for the largest share of the research application subsegment of the oligonucleotide synthesis market. PCR technologies such as real-time PCR or quantitative PCR (qPCR) used for both qualitative and quantitative analysis in the fields of molecular diagnostics, medicine, microbiology, and forensic biology are driving end-user demand. These PCR applications utilize sequence-specific primers, thus boosting the market for oligos (which are used as probes and primers) in the PCR market.

The North America region is expected to show the highest CAGR of the oligonucleotide synthesis market. The growing investments in research and development by major pharmaceutical & biotechnology companies, increasing application of oligonucleotides in pharmaceutical drug research, and growing public & private sector investments in genomics and related technologies are expected to aid market growth in the North America.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=200829350

Oligonucleotide Synthesis Market Dynamics:

Drivers:

- Increasing use of synthesized oligos in therapeutic and diagnostic applications

- Technological advancements

- Growing government investments in life science research and synthetic biology

- Growing focus on precision/personalized medicine

Restraints:

- Complexities associated with therapeutic oligonucleotides

Opportunities:

- Increasing R&D investments by key players in emerging economies

Challenge:

- Lack of standard regulations

- Delivery of oligonucleotide drugs to specific targets

Key Market Players of Oligonucleotide Synthesis Industry:

Some leading players operating in the oligonucleotide synthesis market are Danaher Corporation (US), Thermo Fisher Scientific Inc. (US), Merck KGaA (Germany), Eurofins Scientific (Luxembourg), LGC Limited (UK), Agilent Technologies, Inc. (US), Kaneka Corporation (Japan), Maravai Lifesciences holdings, Inc. (US), Azenta, Inc. (US), Twist Bioscience Corporation (US) and Genscript Biotech Corporation (US). Major players in the oligonucleotide therapeutics market are Biogen Inc. (US), Alnylam Pharmaceuticals, Inc. (US), Sarepta Therapeutics, Inc. (US), Astrazeneca (UK), Astellas Pharma Inc. (Japan), Jazz Pharmaceuticals Plc (Ireland), Nippon Shinyaku, Co. Ltd. (Japan), Ionis Pharmaceuticals, Inc. (US) and Novartis AG (Switzerland).

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side- 70% and Demand Side – 30%

- By Designation: Managers- 45%, CXOs, and Director level – 30%, and Executives – 25%

- By Region: North America -35%, Europe – 25%, Asia-Pacific -15%, Latin America -10%, Middle East- 10%, Africa- 5%

Recent Developments of Oligonucleotide Synthesis Industry:

- In November 2023, LCG Biosearch Technologies, a business unit of LGC Limited, acquired PolyDesign to enhance its oligonucleotide synthesis capabilities using PolyDesign’s frit technology.

- In October 2023, Integrated DNA Technologies (IDT), a subsidiary of Danaher Corporation, opened its therapeutic oligonucleotide manufacturing facility in Coralville, Iowa. This facility will produce reagents for cGMP cell & gene therapy, including single-guide RNAs and HDR donor oligos.

Oligonucleotide Synthesis Market – Key Benefits of Buying the Report:

The report will help market leaders/new entrants by providing them with the closest approximations of the revenue numbers for the overall oligonucleotide synthesis market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to position their business and make suitable go-to-market strategies. This report will enable stakeholders to understand the market’s pulse and provide information on the key market drivers, restraints, challenges, trends, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (e.g., Increasing use of synthesized oligos in therapeutic and diagnostic applications, Technological advancements), restraints (e.g., complexities associated with oligonucleotide-based drugs), opportunities (e.g., increasing pharma R&D investments in emerging economies), and challenges (e.g., lack of standard regulations) are influencing the growth of the oligonucleotide synthesis market.

- Product Approvals: Detailed insights on newly approved products of the oligonucleotide synthesis market.

- Market Development: Comprehensive information about lucrative markets – the report analyses the oligonucleotide synthesis market across varied regions.

- Market Diversification: Exhaustive information about new products, recent developments, and investments in the oligonucleotide synthesis market.

- Pipeline Analysis: Comprehensive information about products under clinical trials.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players including Danaher Corporation (US), Thermo Fisher Scientific Inc. (US), Merck KGaA (Germany), among others offering products for research & diagnostic applications and Biogen Inc. (US), Alnylam Pharmaceuticals, Inc. (US), Sarepta Therapeutics, Inc. (US) among others offering products for therapeutic applications.

Get access to the latest updates on Oligonucleotide Synthesis Companies and Oligonucleotide Synthesis Industry Growth

Content Source: https://www.prnewswire.com/news-releases/oligonucleotide-synthesis-market-worth-19-7-billion–marketsandmarkets-302128509.html

-

Data-Driven Healthcare: The Evolution of Healthcare Analytical Testing Services Market

According to a new report by MarketsandMarkets™ – Healthcare Analytical Testing Services Market in terms of revenue was estimated to be worth $7.4 billion in 2024 and is poised to reach $12.6 billion by 2029, growing at a CAGR of 11.2% from 2024 to 2029.

The expansion of the healthcare analytical testing services market is driven by growing demand across various industries seeking quality assurance and compliance with regulations. Challenges in refining accurate analytical techniques create openings for service providers, while government efforts foster investment and creativity. These dynamics stimulate market growth worldwide, along with trends like outsourcing driven by cost considerations and advancements in pharmaceuticals. Additionally, venturing into new markets increases the demand for tailored testing, further spurring the requirement for Healthcare Analytical Testing Services.

Download an Illustrative overview: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=108923833

The Healthcare Analytical Testing Services market is diversified based on the types of services offered, encompassing cell-based assays, virology testing, biomarker testing, immunogenicity and neutralizing antibody testing, pharmacokinetic testing, and various other bio–Healthcare Analytical Testing Services. Among these, cell-based assays emerged as the dominant segment in 2023. This dominance can be attributed to the increasing utilization of cell-based assays in high-throughput screening processes. Unlike biochemical assays, cell-based assays offer the advantage of providing biologically relevant in vivo information, thereby expediting the drug discovery process. This trend underscores the growing importance of cell-based assays in meeting the demands of pharmaceutical and biotechnology companies for efficient and effective analytical testing

The Healthcare Analytical Testing Services market caters to various end users, including pharmaceutical & biopharmaceutical companies, medical device manufacturers, forensic laboratories, hospitals and clinics, as well as cosmetics and nutraceutical companies. In 2023, pharmaceutical & biopharmaceutical companies emerged as the leading end users, holding the largest market share. This dominance is primarily due to the increasing trend among these companies to outsource their analytical testing needs. By outsourcing, pharmaceutical and biopharmaceutical firms can optimize their resources, streamline operations, and focus more on their core competencies such as research, development, and production. This strategic approach allows them to enhance efficiency, maintain regulatory compliance, and ultimately improve profit margins. As a result, the demand for Healthcare Analytical Testing Services from pharmaceutical and biopharmaceutical companies continues to grow, driving the expansion of this market segment.

The Healthcare Analytical Testing Services market is segmented by region into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Among these regions, North America stands out as the largest contributor to market share. This dominance is primarily driven by the burgeoning presence of biopharmaceutical and pharmaceutical companies, particularly in the United States. The US, being a hub for innovation and research in the healthcare sector, attracts significant investments and fosters the development of advanced analytical testing solutions. Furthermore, the region benefits from the presence of well-established market players with extensive expertise and infrastructure. Their robust capabilities and technological advancements contribute significantly to the growth and sophistication of the Healthcare Analytical Testing Services market in North America. Overall, the region’s favorable regulatory environment, coupled with its focus on quality assurance and compliance, further solidifies its leading position in the global market landscape.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=108923833

Healthcare Analytical Testing Services Market Dynamics:

Drivers:

- Changing regulatory landscape and the increasing complexity of products to drive the market

- Rising number of Clinical Trials

Restraints:

- Lack of skilled professionals

Opportunities:

- Harnessing Government Support and Technology Advancements in Healthcare analytical testing services

Challenge:

- Need for improvement to the sensitivity of analytical testing

Key Market Players of Healthcare Analytical Testing Services Industry:

The prominent players in the global Healthcare Analytical Testing Services market include Eurofins Scientific (Luxembourg), , Thermo Fisher Scientific, Inc. (US), Pace Analytical Services LLC (US), Intertek Group plc (UK), IQVIA Inc. (US), Merck KGaA (Germany), Source BioScience (UK), Almac Group (UK), Laboratory Corporation of America Holdings (US), SGS S.A. (Switzerland), Charles River Laboratories (US), WuXi AppTec Co. Ltd. (China), Element Materials Technology (UK), ICON Plc (Ireland), Frontage Laboratories, Inc. (US), STERIS Plc (US), Sartorius AG (Germany), ALS Life Science (US), Syneos Health, INC (US), Medpace Holdings, Inc. (US), LGC Limited (UK), Parexel International Corporation (US), Celerion (US). Pharmaron (China), and BioAgilytix Labs (US).

The break-down of primary participants is as mentioned below:

- By Company Type – Tier 1: 45%, Tier 2: 30%, and Tier 3: 25%

- By Designation – C-level: 42%, Director-level: 31%, and Others: 27%

- By Region – North America: 32%, Europe: 32%, Asia Pacific: 26%, ROW-10%

Recent Developments of Healthcare Analytical Testing Services Industry:

- In March 2024, Thermo Fisher Scientific Inc. (US), collaborated with Symphogen (US), to provide biopharmaceutical discovery and development laboratories with innovative tools and streamlined workflows for efficient characterization of complex therapeutic proteins

- In February 2024, Charles River Laboratories (US) partnered with Wheeler Bio, Inc. (US). This agreement accelerates the transition from preclinical to early clinical stages for biotech firms, streamlining processes and providing a comprehensive solution.

- In May 2023, Laboratory Corporation of America Holdings (US Collaborated with Forge Biologics (US) to advance gene therapy development and manufacturing. This collaboration aims to expedite clinical timelines, overcome analytical development barriers, and address regulatory hurdles associated with manufacturing and development processes.

- In May 2023, SGS S.A. (Switzerland), SGS SA acquired a majority stake in Nutrasource Pharmaceutical and Nutraceutical Services Inc. (Canada0), Initially acquiring 60% of Nutrasource’s shares, SGS also has the option to acquire the remaining 40% in 2026. This strategic acquisition strengthens SGS’s presence in key market segments and enhances its ability to deliver comprehensive services to clients worldwide.

- In July 2022, Eurofins Scientific (Luxembourg), acquired WESSLING (Hungary), to strengthen its presence in Central and Eastern Europe and to enhance its BioPharma Product Testing capabilities.

Healthcare Analytical Testing Services Market – Key Benefits of Buying the Report:

This report will enrich established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the below-mentioned strategies to strengthen their positions in the market.

This report provides insights on:

- Analysis of Market Dynamics (Stringent regulatory landscape, growing focus on analytical testing of bilogics and biomilars, rising investments in pharma and biopharma R & D), restraints (Increasing Preassure on market players due to rising cost and market competition), opportunities (Adoption of new technologies, supporting government initiatives), and challenges (increasing need for improvement of sentsitivity of bioanalytical methods)

- Services/Innovations: Detailed insights on upcoming technologies, research & development activities, and new service launches in the Healthcare analytical testing services market.

- Market Development: Comprehensive information on the lucrative emerging markets, component, demographics, end-user, and region.

- Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the healthcare analytical testing services market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, and capabilities of the leading players in the healthcare analytical testing services market like Eurofins Scientific (Luxembourg), Laboratory Corporation of America Holdings (US), SGS S.A. (Switzerland), Charles River Laboratories (US), WuXi AppTec Co. Ltd. (China), Element Materials Technology (UK) among others.

Research Insights: https://www.marketsandmarkets.com/ResearchInsight/healthcare-analytical-testing-services-market.asp

Content Source: https://www.marketsandmarkets.com/PressReleases/healthcare-analytical-testing-services.asp

-

Improving Patient Outcomes: The Impact of Clinical Communication and Collaboration Solutions

According to a new report by MarketsandMarkets™ – Clinical Communication & Collaboration Market in terms of revenue was estimated to be worth $2.6 billion in 2024 and is poised to reach $4.8 billion by 2029, growing at a CAGR of 13.2% from 2024 to 2029.

The growth in the clinical communication and collaboration market is driven by high prevalence of chronic diseases, rising prominence of big data and mHelath tools, and stringent regulatory requirements and industry standards. Moreover, transition towards value-based care and population health management further increases the significance of clinical communication and collaboration solutions. Thus, the the growing emphasis on interoperability and data exchange within healthcare ecosystems is expected to drive the integration of clinical communication and collaboration market during the forecast period.

Download an Illustrative overview: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=118830286

On the basis component, the Clinical Communication and Collaboration market is segmented into hardware, software and services segment. The software segment accounted for the largest share of the component segment in 2023. The software segment comprises of clinical alerting & notification, physician & nurse scheduling systems, telehealth platform, collaborative care platforms. The clinical alerting & notification segment held the largest market share in the software segment. These systems plays a pivotal role in enhancing patient safety, as it reduces response times, and improves clinical decision-making. Moreover, the increasing focus on care coordination and continuity across healthcare settings has propelled the demand for robust clinical alerting and notification solutions. Owing to the many benefits of the software solutions, several healthcare providers are increasingly adopting these solutions for smooth workflows and enhanced quality care.

Based on application, the Clinical Communication and Collaboration market is segmented into lab & radiology communication, nurse communication, patient communication & emergency alerts, physician communication. The physician communication segment held the largest market in 2023 due to its pivotal role in facilitating effective care delivery and enhancing care coordination. Moreover, the unique communication needs of physicians, including the requirement for secure and confidential communication channels, further highlights the importance of dedicated physician communication solutions within the clinical communication and collaboration market. These solutions offer encrypted messaging, secure voice and video calling, and other advanced features tailored to the specific requirements of healthcare providers, enabling them to communicate effectively while adhering to stringent privacy and security regulations.

Based on end users, the Clinical Communication and Collaboration market is segmented into hospitals & clinics, ambulatory surgical centers, long-term care facilities, nursing centers and other end-users which includes maternity care centers & fertility centers, and trauma and emergency care centers. The hospitals & clinics held the largest share among the end-users in 2023. From emergency departments and operating rooms to inpatient units and outpatient clinics, healthcare providers in hospitals and clinics rely heavily on effective communication channels to coordinate care plans, consult with colleagues, and ensure continuity of care for patients. As healthcare organizations continue to prioritize communication solutions that enhances care coordination, streamlines workflows, and support remote care delivery, hospitals and clinics are poised to remain key drivers of innovation and growth in the clinical communication and collaboration market.

The Clinical Communication and Collaboration market is segmented into five major regional segments, namely, North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. In 2023, North America accounted for the largest share of the Clinical Communication and Collaboration market. This region’s dominance is due to highly developed healthcare infrastructure characterized by advanced technology adoption, robust regulatory frameworks, and a strong emphasis on patient-centric care delivery. Moreover, the presence of key market players such as Avaya LLC (US), Oracle (US), Cisco Systems, Inc. (US), Microsoft Corporation (US) among others are a key factor contributing to the growth of the region.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=118830286

Clinical Communication & Collaboration Market Dynamics:

Drivers:

- Advantages of clinical communication solutions in enhancing patient care and safety

Restraints:

- High investments required to build IT infrastructure

Opportunities:

- Growing opportunities in emerging markets

Challenge:

- Data security issues

Key Market Players of Clinical Communication & Collaboration Industry:

Prominent players in the Clinical Communication and Collaboration market include Avaya LLC (US), Oracle (US), Cisco Systems, Inc. (US), Microsoft Corporation (US), Baxter International (Hillrom) (US), symplr (US), NEC Corporation (Japan), Spok Inc. (US), Vocera Communications (Stryker) (US), Ascom Holding AG (Switzerland), Everbridge (US), Hidden Brains InfoTech. (India), Imprivata, Inc. (US), CommuniCare Technology, Inc. d/b/a Pulsara (US), Mobile Heartbeat (C-HCA, Inc.) (US), OnPage. (US), HARRIS ONPOINT (US), Jive Software, LLC (US), TigerConnect (US), JCT Healthcare Pty Ltd. (Australia), Amplion (US), AndorHealth (US), PerfectServe, Inc. (US), QliqSOFT, Inc. (US), and Connexall, GlobeStar Systems Inc. (Canada).

Breakdown of supply-side primary interviews, by company type, designation, and region:

- By Company Type: Tier 1 (40%), Tier 2 (35%), and Tier 3 (25%)

- By Designation: C-level (35%), Director-level (45%), and Others (20%)

- By Region: North America (55%), Europe (20%), Asia Pacific (15%), Latin America (5%) and Middle East Africa (5%)

Recent Developments of Clinical Communication & Collaboration Industry:

- In September 2023, Microsoft Corporation (US) collaborated with Mercy (US) to enable clinicians to revolutionize patient care through the use of generative AI.

- In August 2023, TeleVox (US) partnered with Oracle (US) to enhance its patient engagement solutions, leveraging OCI’s platform for improved communication in healthcare. As part of the Oracle PartnerNetwork (OPN), TeleVox on OCI delivers advanced capabilities for healthcare practices.

- In April 2023, Mobile Heartbeat (US) partnered with Akkadian Labs, LLC. (US) a leading developer of unified communications (UC) provisioning automation solutions. With this partnership, Mobile Heartbeat and Akkadian Labs aim to empower healthcare organizations with enhanced communication and collaboration capabilities, ultimately improving patient care outcomes.

Research Insights: https://www.marketsandmarkets.com/ResearchInsight/clinical-communication-collaboration-market.asp

Content Source: https://www.marketsandmarkets.com/PressReleases/clinical-communication-collaboration.asp

-

Improving Comfort, Ensuring Compliance: Sleep Apnea Oral Appliances Market Trends

According to a new report by MarketsandMarkets – Sleep Apnea Oral Appliances Market in terms of revenue was estimated to be worth $0.4 billion in 2023 and is poised to reach $0.9 billion by 2028, growing at a CAGR of 15.2% from 2023 to 2028. The growth of this market is majorly driven by the high risk of growing awarrness and diagnosis of sleep apnea among patients and healthcare professionals. Furthermore, the poor compliance associated with CPAP is expected to drive the growth of the sleep apnea oral appliances market.

Download an Illustrative overview: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=105423877

Mandibular advancement devices force the lower jaw forward and downwards slightly, which keeps the airway open. The device helps treat OSA by offering maximum anterior tongue space along with the retention of teeth movement. This segment is expected to dominate the global sleep apnea oral appliances market during the forecast period, driven by a rising patient preference for non-CPAP solutions due comfort and ease of use.

By end user, the global sleep apnea oral appliances market is broadly segmented into home care settings/individuals, hospitals, and dental clinics. The large share of this segment can be attributed to factors such as the increasing number of sleep centers globally, the rise of number of sleep care devices for homecare settings offered by leading players.

Based on the region, the sleep apnea oral appliances market is segmented into North America, Europe, Asia Pacific, and the Rest of the World. The North American market is driven by high prevalence and diagnosis of sleep apnea in the region. Europe is the second-largest market for the sleep apnea oral appliances market due to the growing aging population in the region. Asia Pacific will observe high growth during the forecast period with its growing healthcare expenditure with improving accessibility to sleep clinics and treatment for sleep apnea in the region’s countries.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=105423877

Sleep Apnea Oral Appliances Market Dynamics:

Drivers:

- Large pool of undiagnosed sleep apnea patients

Restraints:

- Associated risks of oral appliances for obstructive sleep apnea treatment

Opportunities:

- Poor compliance associated with CPAP

Challenge:

- Expenses associated with customization of oral appliances

Key Market Players of Sleep Apnea Oral Appliances Industry:

Major players in the sleep apnea oral appliances market include SonmoMed (Australia), resMed (US), Whole You, Inc. (US), ProSomnus Sleep Technologies (US), and Vivos Therapeutics, Inc. (US).

Breakdown of supply-side primary interviews, by company type, designation, and region:

- By Company Type: Tier 1 (40%), Tier 2 (50%), and Tier 3 (10%)

- By Designation: C-level (48%), Director-level (37%), and Others (15%)

- By Region: North America (56%), Europe (20%), Asia- Pacific (17%), and Rest of the World (7%)

Sleep Apnea Oral Appliances Market Recent Developments:

- In 2023, Vivos Therapeutics, Inc. (US) DNA appliance was granted 510(k) clearance from the U.S. Food & Drug Administration (or FDA) as a Class II medical device in December 2022 for the treatment of snoring and mild to moderate OSA in adults.

- In 2022, ResMed (US) acquired the German-based clinical, financial, and operational solutions provider MEDIFOX DAN (Germany) to drive leadership in out-of-hospital software solutions.

- In 2021, SomoMed (Australia) conducted SomSUMMIT ’21, which aimed to enhance research, education, and awareness of oral appliance therapy as a primary solution to successful OSA treatment.

Sleep Apnea Oral Appliances Market – Key Benefits of Buying the Report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall sleep apnea oral appliance market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (large pool of undiagnosed sleep apnea patients, growing awareness of effects of untreated sleep apnea, growing usage of oral appliance), restraints (high prices of customized oral appliances, alternative therapies and medications, risks associated with oral appliance therapy for obstructive sleep apnea), opportunities (growing demand for home sleep apnea tests, increasing focus on telemedicine, mHealth, and AI, poor compliance associated with CPAP), and challenges (complex referral pathways and long waiting periods) influencing the growth of the sleep apnea oral appliance market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the sleep apnea oral appliance market.

- Market Development: Comprehensive information about lucrative markets – the report analyses the sleep apnea oral appliance market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the sleep apnea oral appliance market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like SomnoMed (Australia), ResMed (US), and ProSomnus Sleep Technologies (US), among others in the sleep apnea oral appliance market strategies.

Research Insight: https://www.marketsandmarkets.com/ResearchInsight/sleep-apnea-oral-appliances-market.asp

Content Source: https://www.marketsandmarkets.com/PressReleases/sleep-apnea-oral-appliances.asp

-

Future Outlook of the Endoscopy Equipment Market: Emerging Technologies and Market Expansion

According to a new report by MarketsandMarkets™. – Endoscopy Equipment Market in terms of revenue was estimated to be worth $32.3 billion in 2024 and is poised to reach $46.2 billion by 2029, growing at a CAGR of 7.4% from 2024 to 2029.

The growth in this market is primarily driven by factors such as increasing prevalence of gastrointestinal diseases, rising demand for minimally invasive surgeries, technological advancements leading to enhanced imaging and procedural capabilities, expanding healthcare infrastructure, and growing awareness about early disease diagnosis and treatment.

Download an Illustrative overview: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=689

In the forecast period, the endoscopes segment dominated the global endoscopy equipment market. This significant share can be credited to the increasing favouritism of minimally invasive procedures by both patients and healthcare professionals, along with the elevated uptake of such equipment by end users. Moreover, continuous advancements in endoscopy technologies contribute to the segment’s substantial presence in the market.

Based on application, the obstetrics/gynecology endoscopy segment of the endoscopy equipment market accounted the third largest market share in the forecast period. This growth subjected to the rising incidence of gynaecological conditions like endometriosis, uterine fibroids. Technological improvements in visualization systems and endoscopes, accessories tools like grasping tools are driving the growth of the gynecology endoscopy segment as well.

Ambulatory surgery centers/clinics secure the second-largest market share in the endoscopy equipment market. This largest share comes from the increasing trend towards outpatient procedures due to their convenience and cost-effectiveness. Additionally, the rising demand for minimally invasive surgeries in these settings drives the adoption of advanced endoscopy equipment. As ambulatory surgery centers continue to grow in popularity, the demand for endoscopy equipment in these facilities is expected to witness steady growth in the foreseeable future.

Europe to possess the second largest market share in the endoscopy equipment market in the forecast period due to its rising investments towards medical technology, high adoption rates of advanced medical technologies, and increasing prevalence of gastrointestinal diseases. These factors drive demand for endoscopy equipment, positioning Europe as one of the leading market regions.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=689

Endoscopy Equipment Market Dynamics:

Drivers:

- Growing focus of hospitals to invest in technologically advanced endoscopy instruments and expand endoscopy units

Restraints:

- High overhead costs of endoscopy procedures with limited reimbursement in developing countries

Opportunities:

- Booming healthcare sector in developing economies

Challenge:

- Shortage of trained physicians and endoscopicts

Key Market Players of Endoscopy Equipment Industry:

Prominent players in the endoscopy equipment market include Olympus Corporation (Japan), KARL STORZ SE & Co. KG (Germany), Boston Scientific Corporation (US), JOHNSON & JOHNSON (US), Stryker Corporation (US), Medtronic, plc (Ireland), Fujifilm Holdings Corporation (Japan), HOYA Corporation (Japan), Nipro Corporation (Japan), Smith & Nephew plc (UK), Intuitive Surgical, Inc. (US)

A breakdown of the primary participants (supply side) for the endoscopy equipment market referred to for this report is provided below:

- By Company Type: Tier 1–35%, Tier 2–20%, and Tier 3–45%

- By Designation: C-level–45%, Director Level–25%, and Others–30%

- By Region: North America–36%, Europe–26%, Asia Pacific–21%, Latin America-10%, and Middle East & Africa_ 7%

Recent Developments of Endoscopy Equipment Industry:

- In November 2023, Olympus Corporation launched the EVIS X1, an advanced endoscopy system in the existing product portfolio of the company.

- In September 2023, Stryker launched, 1788, a minimally invasive surgical camera, offering more vibrant image with balanced lighting.

- In January 2022, The Johnson & Johnson Medical Devices Companies (JJMDC) collaborated with Microsoft Corporation Inc, (US) to enable and expand JJMDC’s secure and compliant digital surgery ecosystem.

Get 10% Free Customization on this Report: https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=689

Endoscopy Equipment Market – Key Benefits of Buying the Report:

The study will assist industry leaders/new entrants in this market by providing information on the closest approximations of the endoscopic equipment market and its segments. This research will assist stakeholders understand the competitive landscape, obtain insights to better position their firms, and develop appropriate go-to-market strategies. The study will also assist stakeholders in understanding the market pulse and obtaining information on major market drivers, constraints, opportunities, and challenges.

This report provides insights into the following pointers:

- Analysis of key Drivers: Drivers (rising requirement for endoscopy to diagnose and treat target diseases, increasing investments, funds, and grants by governments and other organizations, growing focus of hospitals to expand endoscopic units, ongoing advancements in endoscopic technologies, rising incidence of inflammatory bowel disease and colorectal cancer, increasing preference for minimally invasive surgeries, higher adoption of single-use endoscopy instruments, rising focus of medical specialists to shift from manual to automated endoscopy reprocessing), Restrains (unfavourable healthcare reforms in US, high overhead costs of endoscopy procedures with limited reimbursement in emerging economies, high risk of getting viral infections during endoscopic procedures), Opportunities (rapidly developing healthcare sector in emerging economies), Challenges (increasing number of product recalls, lack of proper sterilization and reprocessing, shortage of trained physicians and endoscopists) influencing the growth of the endoscopy equipment market.

- Market Penetration: Comprehensive information on the product portfolios of the leading companies in the endoscopic equipment market. The report breaks down the market by product type, end user, and region.

- Product Enhancement/Innovation: Detailed information about forthcoming trends and product launches in the endoscopic equipment market.

- Market Development: Comprehensive data on attractive rising markets broken down by product category, application, end user, and region

- Market Diversification: Comprehensive information on new products, expanding geographies, current advancements, and investments in the endoscopic equipment market.

- Competitive Assessment: In-depth analysis of market share, growth strategies, product and service offerings, and capabilities of the main endoscopic equipment manufacturers.

Research Insights: https://www.marketsandmarkets.com/ResearchInsight/endoscopy-devices-market.asp

Content Source: https://www.marketsandmarkets.com/PressReleases/endoscopy.asp

-

Precision Oncology and Beyond: The Impact of Companion Diagnostics

According to a new report by MarketsandMarkets™ – Companion Diagnostics Market in terms of revenue was estimated to be worth $7.5 billion in 2024 and is poised to reach $13.6 billion by 2029, growing at a CAGR of 12.6% from 2024 to 2029.

The global companion diagnostics market is poised for significant growth in the near future, driven by the increasing incidence of cancers worldwide. This rise in cancer cases is fueling the demand for more accurate and personalized treatment options. Companion diagnostics play a crucial role in this scenario by helping to select appropriate targeted therapies for patients based on their genetic makeup and likely response. This personalized approach is expected to improve treatment outcomes while reducing adverse reactions to unsuited medicines. Additionally, the approvals of many targeted oncology drugs, along with complementary companion diagnostics, by regulatory agencies are expected to further propel the market growth. Emerging economies like China, Japan, and India are presenting attractive opportunities for companies operating in this market.

Download an Illustrative overview: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=155571681

Based on product & service, the companion diagnostics market is segmented into assays, kits & reagents, instruments/systems and software & services. The dominance of the assays, kits & reagents segment in 2023 can be attributed primarily to the broad range of available products and the rapidly increasing utilization of assays and kits across various therapeutic areas.

Based on technology, the companion diagnostics market is categorized into polymerase chain reaction (PCR), in situ hybridization (ISH), next-generation sequencing (NGS), immunohistochemistry (IHC), and other technologies. In 2023, the PCR segment held the largest portion of the companion diagnostics market. PCR has become essential in companion diagnostics, especially in the interpretive practice by pharmaceutical companies related to oncology drugs, due to its reliability, sensitivity, and ability to obtain quantitative results. Its extensive range of applications and established market presence give it a significant position in the field.

Based on indication, the companion diagnostics market is segmented into cancer, cardiovascular diseases (CVDs), neurological diseases, infectious diseases, and other indications (inflammatory and inherited diseases, among others). In 2023, the cancer segment held the largest share of the companion diagnostics market. This can be attributed to factors such as the expanding role of companion diagnostics in personalized medicine treatments for cancer, as well as the growing importance of biomarkers in cancer diagnosis.

Based on sample type, the companion diagnostics market is segmented into liquid, blood, and other sample types. In 2023, the tissue sample segment accounted for the largest share of the companion diagnostics market. Tissue samples are often preferred in companion diagnostics for their ability to provide a direct analysis of the tumor, offering a comprehensive view of genetic mutations and biomarkers for more accurate and personalized treatment decisions.

Based on end user, the companion diagnostics market is segmented into pharmaceutical & biotechnology companies, reference laboratories, CROs, and other end users (including physician & hospital laboratories and academic medical centers). The pharmaceutical & biotechnology companies segment held the largest share of the companion diagnostics market in 2023. This is primarily driven by factors such as the rising utilization of companion diagnostics in drug development and the growing significance of companion diagnostic biomarkers.

The global companion diagnostics market is divided into six key regions: North America, Europe, Asia Pacific, Latin America, the Middle East & Africa, and GCC countries. In 2023, North America held the largest portion of the companion diagnostics market. The growth of the North American companion diagnostics market can be credited to several factors, including the significant presence of leading companion diagnostics vendors and national clinical laboratories. Additionally, the easy access to technologically advanced devices and instruments, along with the highly developed healthcare systems in the US and Canada, contributed to the market’s expansion in this region.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=155571681

Companion Diagnostics Market Dynamics:

Drivers:

- Increasing significance of personalized medicine

Restraints:

- High capital investment and low cost-benefit ratio

Opportunities:

- Increasing importance of companion diagnostics in drug development

Challenge:

- The shortage of adequately trained professionals

Key Market Players of Companion Diagnostics Industry:

The major players in this market are F. Hoffmann-La Roche Ltd (Switzerland), Agilent Technologies, Inc. (US), QIAGEN (Netherlands), Thermo Fisher Scientific Inc. (US), Abbott (US), Almac Group (UK), Danaher (US), Illumina, Inc. (US), bioMérieux (France), Myriad Genetics, Inc. (US), Sysmex Corporation (Japan), ARUP Laboratories (UK), Abnova Corporation (Taiwan), Guardant Health (US), ICON Plc (Ireland), BioGenex (US), Invivoscribe, Inc. (US), ArcherDX, Inc. (Integrated DNA Technologies, Inc.) (US), NG Biotech (France), Q² Solutions (US), Amoy Diagnostics Co., Ltd. (China), Uniogen (Abacus Diagnostica) (Finland), Asuragen, Inc. (Bio-Techne) (US), NG Biotech (France), Meso Scale Diagnostics, LLC. (US), and Creative Biolabs (US).

The primary interviews conducted for this report can be categorized as follows:

- By Company Type: Tier 1 – 20%, Tier 2 – 45%, and Tier 3 -35%

- By Designation: C-level – 30%, D-level – 20%, and Others – 50%

- By Region: North America – 42%, Europe – 31%, Asia Pacific – 20%, and Rest of the World -7%

Recent Developments of Companion Diagnostics Industry:

- In August 2023, Agilent Technologies, Inc. (US) received European IVDR Certification for Companion Diagnostic Assay.

- In August 2023, QIAGEN (Netherlands). received FDA approval for companion diagnostic to Blueprint Medicines’ AYVAKIT (avapritinib) in gastrointestinal stromal tumors.

- In March 2023, F. Hoffmann-La Roche Ltd (Switzerland) received FDA approval of label expansion for VENTANA PD- L1 (SP263) Assay to identify patients with locally advanced and metastatic non-small cell lung cancer eligible for Libtayo.

- In September 2022, Thermo Fisher Scientific Inc. (US) announced FDA Approval of Oncomine Dx Target Test as the First NGS-Based Companion Diagnostic to Aid in Therapy Selection for Patients with RET Mutations/Fusions in Thyroid Cancers.

- In January 2021, F. Hoffmann-La Roche Ltd (Switzerland) launched two digital pathology image analysis algorithms for precision patient diagnosis in breast cancer.

Companion Diagnostics Market – Key Benefits of Buying the Report:

The report will help market leaders/new entrants by providing them with the closest approximations of the revenue numbers for the overall companion diagnostics market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to better position their business and make suitable go-to-market strategies. This report will enable stakeholders to understand the market’s pulse and provide them with information on the key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers, restraints, opportunities, and challenges influencing the growth of the companion diagnostics market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the companion diagnostics market.

- Market Development: Comprehensive information about lucrative markets – the report analyses the companion diagnostics market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the companion diagnostics market.

- Competitive Assessment: In-depth assessment of market ranking, growth strategies and product offerings of leading players like F. Hoffmann-La Roche Ltd (Switzerland), Agilent Technologies, Inc. (US), QIAGEN (Netherlands), Thermo Fisher Scientific Inc. (US) and Abbott (US).

Research Insights: https://www.marketsandmarkets.com/ResearchInsight/companion-diagnostics-market.asp

Content Source: https://www.marketsandmarkets.com/PressReleases/companion-diagnostics.asp

-

Driving Forces in Optometry Equipment: Market Trends and Growth Factors

According to a new report by MarketsandMarkets™ – Optometry Equipment Market in terms of revenue was estimated to be worth $4.5 billion in 2024 and is poised to reach $6.1 billion by 2029, growing at a CAGR of 6.4% from 2024 to 2029.

The principal drivers propelling the expansion of this market are the growing prevalence of eye illnesses, advancements in ophthalmic device technology, expanding government initiatives aimed at preventing visual impairment, growing healthcare expenses, and rising disposable incomes. Companies in the market for optometry equipment are finding that developing nations like China, Japan, and India provide attractive opportunities.

Download an Illustrative overview: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=14475790

According to product type, the worldwide optometry equipment market is divided into three segments: goods for general examinations, cornea and cataract examinations, and products for glaucoma and retinal examinations. In2023, the optometry equipment market was dominated by the sector that produced examination goods for glaucoma and retina. The significant portion of the market is due to a variety of factors, including the expansion of clinics, the increasing incidence of glaucoma and retinal disorders, the easier availability to modern ophthalmic diagnostic technologies, and technological advancements in optometry equipment.

The market for optometry equipment is divided into segments based on applications, including age-related macular degeneration, cataract surgery, glaucoma, and general exams. As of 2023, the worldwide optometry equipment market was dominated by the general examination segment. The primary factors influencing this segment’s size include the aging population, the rise in the prevalence of eye diseases, and the number of cases of diabetes and hypertension.

By end user, the optometry equipment market is divided into eye clinics, hospitals, and other consumers. The sector that held the biggest share of the global optometry equipment market in 2023 was clinics. This sector makes up a sizeable share of the market because of the vast number of patients treated in clinics and the increasing number of private clinical practices founded by ophthalmologists in emerging countries.

There are five main regions that make up the global market for optometry equipment: North America, Europe, Asia Pacific, and Rest of the World (which includes Latin America, the Middle East & Africa, and GCC countries). In terms of market share, North America led the optometry equipment market in 2023. Some of the contributing factors are the rising prevalence of ocular diseases, the rapidly aging population, the accessibility of state-of-the-art optometry equipment, and the growing utilization of ophthalmology procedures and therapies in this field.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=14475790

Optometry Equipment Market Dynamics:

Drivers:

- Increasing incidence of eye disorders

- Cataracts

- Glaucoma

- Technological advancements in ophthalmic devices

- Rising government initiatives to control visual impairment

- Increasing healthcare expenditure

Restraints:

- High cost of optometry equipment

- Growing adoption of refurbished optometry equipment

Opportunities:

- Growth opportunities in emerging markets

Challenge:

- Growth opportunities in emerging markets

Key Market Players of Optometry Equipment Industry:

The major players leading in optometry equipment market are Carl Zeiss Meditec AG (Germany), EssilorLuxottica (France), Alcon (Switzerland), Topcon Corporation (Japan), Bausch Health Companies Inc. (Canada), NIDEK Co. Ltd. (Japan), Canon Inc. (Japan), Johnson and Johnson (US), HEINE Optotechnik (Germany), Revenio Group PLC (Finland), Haag-Streit Group (Switzerland) and Heidelberg Engineering (Germany).

Breakdown of supply-side primary interviews, by company type, designation, and region:

- By Company Type: Tier 1 (40%), Tier 2 (30%), and Tier 3 (30%)

- By Designation: C-level (27%), Director-level (18%), and Others (55%)

- By Region: North America (51%), Europe (21%), Asia- Pacific (18%), Latin America (6%), and Middle East & Africa(4%)

Recent Developments of Optometry Equipment Industry:

- In August 2023, Carl Zeiss launched the ZEISS trifocal technology on a glistening-free hydrophobic C-loop platform and a fully preloaded injector for safe and reliable implantation.

- In March 2022, Topcon Corporation launched SOLOS, an automatic lens analyzer that enables advanced, accurate, and efficient lens analysis at the touch of a button.

- In September 2023, Bauch + Lomb acquired XIIDRA to grow in the prescription dry eyes segment.

- In January 2023Bausch + Lomb acquired AcuFocus to expand its cataract surgical portfolio.

Optometry Equipment Market – Key Benefits of Buying the Report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall optometry equipment market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and to plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (High prevalence of eye diseases, growing geriatric population), restraints (High Cost and use of refurbished equipments), opportunities (Rising healthcare expenditure, Increasing Demand from Emerging Economies), and challenges (low awareness, limited insurance coverage) influencing the growth of the optometry equipment market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the optometry equipment market

- Market Development: Comprehensive information about lucrative markets – the report analyses the optometry equipment market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the optometry equipment market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Carl Zeiss Meditec AG (Germany), EssilorLuxottica (France), Alcon (Switzerland), Topcon Corporation (Japan) and Bausch Health Companies Inc. (Canada), among others in optometry equipment market.

Research Insights: https://www.marketsandmarkets.com/ResearchInsight/optometry-eye-exam-equipment-market.asp

Content Source: https://www.marketsandmarkets.com/PressReleases/optometry-eye-exam-equipment.asp

- Increasing incidence of eye disorders

-

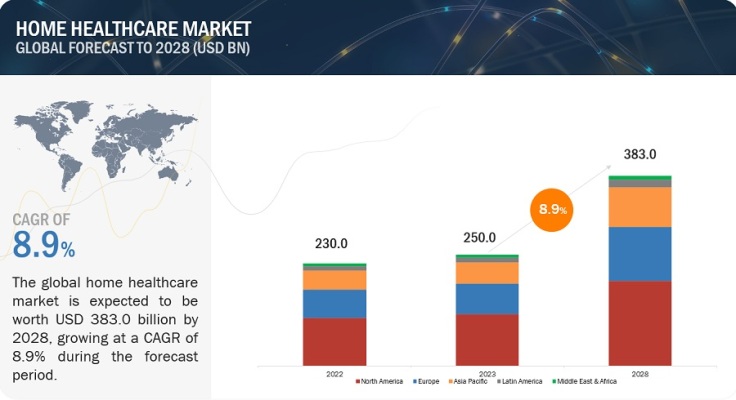

Redefining Healthcare Access: The Role of Home Healthcare

Home Healthcare Market in terms of revenue was estimated to be worth $250.0 billion in 2023 and is poised to reach $383.0 billion by 2028, growing at a CAGR of 8.9% from 2023 to 2028 according to a new report by MarketsandMarkets™. The primary drivers propelling the growth of this market are the aging population, rising healthcare expenditures, and the increased need for home care due to technological advancements in home healthcare.

Download an Illustrative overview: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=696

The home healthcare market is segmented into testing, screening, and monitoring products; therapeutic products; and mobility care products. In 2022, the home healthcare market will be dominated by therapeutic items, primarily because chronic illnesses like diabetes, cancer, and kidney failure are becoming more common.

The home healthcare market on the basis of service is divided into skilled nursing services, rehabilitation therapy services, hospice & palliative care services, unskilled care services, respiratory therapy services, infusion therapy services, and pregnancy care services. Skilled nursing services have the biggest market share for home healthcare in 2022. The industry is expanding due to factors including the aging population.

On the basis of the indication, the home healthcare market has been segregated into cancer, respiratory diseases, movement disorders, cardiovascular diseases & hypertension, pregnancy, wound care, diabetes, hearing disorders, and other indications. By 2022, the home healthcare market’s greatest share belonged to the other indications category. The growing older population and kidney problems are the main factors propelling this market’s expansion.

The global home healthcare market is segmented into four major regions—North America, Europe, the Asia Pacific, and Rest of the World. North America held the biggest market share for home healthcare in 2022. Due to its high disposable income and growing senior population, North America accounts for a sizable portion of the global industry. On the other hand, throughout the course of the forecast period, the Asia Pacific market is anticipated to develop at the highest CAGR. Rising disposable income and government initiatives to promote home healthcare are the main factors driving growth in the Asia Pacific home healthcare industry.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=696

Home Healthcare Market Dynamics:

Drivers:

- Rapid growth in elderly population and rising incidence of chronic diseases

- Rising R&D investments

- Need for cost-effective healthcare delivery due to rising costs

- Increased preference for personalized care

Restraint:

- Changing reimbursement policies

- Limited insurance coverage

- Patient safety concerns

Opportunities:

- Rising focus on telehealth

- Untapped developing regions

- Growing demand for home-use therapeutic devices

- Growing demand for home sleep apnea tests

- Rising preference for home hemodialysis treatment

Challenge:

- Shortage of home care workers

- Lack of supporting infrastructure

Key Market Players of Home Healthcare Industry:

The major players operating in home healthcare market are Fresenius SE & Co. KGaA (Germany), Abbott (US), Koninklijke Philips N.V. (Netherlands), GE Healthcare (US), ResMed, Inc. (US), Linde, Plc (Ireland), F.Hoffmann-La Roche, Ltd. (Switzerland), A&D Company, Limited (Japan), Bayada Home Health Care (US), Invacare Corporation (US), Amedisys (US), LHC Group, Inc. (US), Omron Corporation (Japan), Drive Devilbiss Healthcare (UK), Hamilton Medical (Switzerland), Sunrise Medical (Germany), Roma Medical (UK), Caremax Rehabilitation Equipment Co., Ltd. (China), Vitalograph (UK), Advita Pflegedienst Gmbh (Germany), Renafan Gmbh (Germany), ADMR (France), Apex Medical Corp. (Taiwan), Contec Medical Systems Co., Ltd. (China), Löwenstein Medical Technology Gmbh + Co., KG. (Germany), B. Braun Melsungen Ag (Germany), Baxter International, Inc. (US), Allied Healthcare Products, Inc. (US), Medline Industries, Inc. (US), and Advin Health Care (India).

Breakdown of supply-side primary interviews, by company type, designation, and region:

- By Company Type: Tier 1 (40%), Tier 2 (30%), and Tier 3 (30%)

- By Designation: C-level (27%), Director-level (18%), and Others (55%)

- By Region: North America (51%), Europe (21%), Asia- Pacific (18%), Latin America (6%), and Middle East & Africa (4%)

Home Healthcare Market – Key Benefits of Buying the Report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall home healthcare market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and to plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (High prevalence of chronic diseases, growing geriatric population), restraints (Alternative Technologies), opportunities (Rising healthcare expenditure, Increasing Demand from Emerging Economies), and challenges (stringent regulations, limited insurance coverage) influencing the growth of the home healthcare market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the home healthcare market

- Market Development: Comprehensive information about lucrative markets – the report analyses the home healthcare market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the home healthcare market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Fresenius SE & Co. KGaA (Germany), Abbott (US), GE HealthCare (US), Koninklijke Phillips NV. (Netherlands), ResMed, Inc. (US), among others in home healthcare market.

Research Insights: https://www.marketsandmarkets.com/ResearchInsight/home-healthcare-equipment-market.asp

Content Source: https://www.marketsandmarkets.com/PressReleases/home-healthcare.asp

-

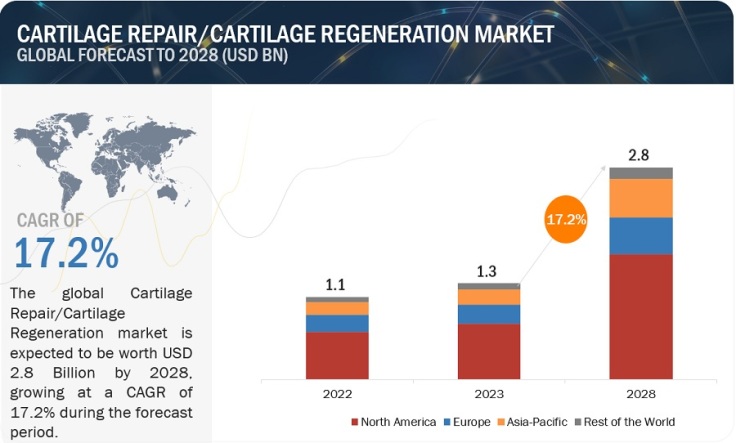

Strategies for Success in the Cartilage Repair Market: Insights and Analysis

Cartilage Repair Market / Cartilage Regeneration market in terms of revenue was estimated to be worth $1.3 Billion in 2023 and is poised to reach $2.8 Billion by 2028, growing at a CAGR of 17.2% from 2023 to 2028 according to a latest report published by MarketsandMarkets™. Growth in the Cartilage Repair/Cartilage Regeneration market is mainly driven by the Increasing incidence of osteoarthritis, increasing research funding and investments and the Rising number of sports and accident-related orthopaedic injuries expected to grow the market demand Cartilage Repair/Cartilage Regeneration market during the forecast period.

Download an Illustrative overview: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=37493272

Based on the treatment modality, the cartilage repair/cartilage regeneration market is divided into two categories which are cell-based including chondrocyte transplantation, growth factors, and stem cells and non-cell-based like tissue scaffolds and cell-free composites. In 2022, the cell-based segment had the largest share in the treatment modality segment which is mainly due to advancements in stem cell- therapies used for cartilage repair.

Based on the Application site, the cartilage repair/cartilage regeneration market is categorized into knees, hips, ankles & feet, and other application sites like nose and shoulder. In 2022, The knee segment holds the largest share of the cartilage repair/cartilage regeneration market. The factors responsible for the growth of the segment are the increasing number of knee arthroscopy procedures and the rising incidence of knee osteoarthritis cases globally.

Based on the Application, the global cartilage repair/cartilage regeneration market is broadly segmented into hyaline cartilage and fibrocartilage. The hyaline cartilage segment accounted for the largest share of the cartilage repair and regeneration market in 2022. Hyaline cartilage is expected to grow highest in the upcoming years due to the increasing number of cartilage repair procedures performed worldwide is the major factor driving the growth of this application segment. Technological advancements, product developments and launches, and growing partnerships between key market players and hospitals are also supporting market growth.

Based on the region segmentation, the cartilage repair/cartilage regeneration market is divided into North America, Europe, Asia Pacific, and the Rest of the World. North America holds the largest share and expects to dominate the cartilage repair/cartilage regeneration market. Growth in the North American market is mainly driven by the rising growth opportunities in emerging economies and growing number of contracts and agreements between market players.

Cartilage Repair Market / Cartilage Regeneration market major players covered in the report, such as:

- Smith+Nephew (UK)

- DePuy Synthes (Johnson & Johnson) (US)

- Zimmer Biomet Holdings, Inc. (US)

- Stryker Corporation (US)

- Vericel Corporation (US)

- B. Braun Melsungen AG (US)

- Anika Therapeutics (US)

- CONMED Corporation (US)

- MEDIPOST (South Korea)

- RTI Surgical (US)

- Arthrex, Inc. (US)

- Regrow Biosciences (India)

- Geistlich Pharma AG (Switzerland)

- AlloSource (US)

- Orthocell Ltd, (Australia)

- Matricel GmbH (Germany)

- CartiHeal, Inc. (Israel)

- Regentis Biomaterials (Israel)

- Theracell Advanced Biotechnology (Greece)

- LifeNet Health (US)

- and Among Others

Request for FREE Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=37493272

This research report categorizes the cartilage repair/cartilage regeneration market into the following segments and subsegments:

Regional Split

- North America

- Europe

- Asia Pacific

- Rest of the World

Treatment Modality Split

- Cell-based

- Chondrocyte Transplantation

- Stem Cells

- Growth Factors

- Non-cell-based

- Tissue Scaffolds

- Cell-free Composites

Application Split

- Knee

- Hip

- Ankle and Foot

- Other Application Sites

Application Site Split

- Hyaline Cartilage

- Fibrocartilage

Key Market Stakeholders:

- Senior Management

- End User

- Finance/Procurement Department

- R&D Department

Report Objectives:

- To provide detailed information about the factors influencing the market growth (such as drivers, restraints, opportunities, and challenges)

- To define, describe, segment, and forecast the cartilage repair/cartilage regeneration market by Product, Application, Medical specialty and Region

- To analyze market opportunities for stakeholders and provide details of the competitive landscape for key players

- To analyze micro markets with respect to individual growth trends, prospects, and contributions to the overall cartilage repair/cartilage regeneration market

- To forecast the size of the cartilage repair/cartilage regeneration market in four main regions along with their respective key countries, namely, North America, Europe, the Asia Pacific, and Rest of the world

- To profile key players in the cartilage repair/cartilage regeneration market and comprehensively analyze their core competencies and market shares

- To track and analyze competitive developments, such as acquisitions; product launches; expansions; collaborations, agreements, & partnerships; and R&D activities of the leading players in the cartilage repair/cartilage regeneration market.

- To benchmark players within the cartilage repair/cartilage regeneration market using the Competitive Leadership Mapping framework, which analyzes market players on various parameters within the broad categories of business and product strategy.

Research Insight: https://www.marketsandmarkets.com/ResearchInsight/cartilage-repair-regeneration-market.asp

Content Source: https://www.marketsandmarkets.com/PressReleases/cartilage-repair-regeneration.asp

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.